Models

Discounted Cash Flow Models

Key Value Driver Model Free Cash Flow Model Forward Market Multiple

Economic Profit Model Adjusted Present Value Model

Artistry and Interpretation in Finance[1]

Valuation modeling is as much of an art as it is a science. While the equations used in motivating model outcomes are all very specific, the construction of the inputs to these models may be less so. Similarly, the outcome of one model given a set of firm inputs may result in an altogether different value than that of another model using inputs for the same firm. If these two models are intended to provide a value relatable to the firm’s Enterprise Value, how is it the outcomes are often so different?

The answer may rest on what the model’s outcome is intended to represent. Consider the Adjusted Present Value (APV) and Key Value Driver (KVD) models. Both rely on the present value of the firm’s future cash flows, which have been adjusted (discounted) to reflect time and some notion of the opportunity cost of capital. The APV model considers a firm’s value as a function of its Free Cash Flow (FCF) plus its Tax Shield (TS), suggesting a firm’s value may be influenced by the firm’s capital structure. The KVD model informs us of the firm’s value as a function of its Net Operating Profit Less Adjusted Taxes (NOPLAT) and its Return on Invested Capital. Supposing both models share all other inputs with equal measures, we might expect the two outcomes to be similar, but they often are not…. that is, unless some very intuitive adjustments are made to reconcile them[2].

It’s possible the outcome differences are simply a function of the algebra underlying the models. Four of the five valuation models under examination in this study employ similar denominators in their continuation forms in which the expected long-run growth rate of the firm’s cash flow (g) is subtracted from the firm’s Weighted Average Cost of Capital (WACC). In the event WACC < g, the value of this term will be expressly negative and may result in a negative overall valuation for the firm, even if the firm has a substantial Enterprise Value and consistently posts significant annual profits. While we may be left to consider whether or not the expected value of g is appropriate, it’s altogether likely we can’t consider these model forms as offering credible outcomes for firms with this problematic relationship between WACC and g.[3]

There’s also the issue of what John Maynard Keynes refers to as Animal Spirits [4] reflected in the market values of both a firm’s equity and debt components at any particular point in time. Based on the notion that a firm’s value to its debt and equity stakeholders is the present value of their claims on the firm’s future cash flows, which is the value most models seek to present, we would expect the value represented by any particular valuation model outcome would equal the firm’s Enterprise Value, or the sum of the market value of its capital components. However, we observe that Enterprise Value and the firm’s calculated values may differ substantially due to short-term economic conditions and their influence on investor demands (Animal Spirits).

Similarly, differences in these measures may also be a function of the effects of asymmetric information held by buyers, sellers, industry analysts, and firm managers with respect to a firm’s capital components in these same markets. For example, when the discount rate applied to the firm by would be investors is not aligned with the discount rate applied by the firm’s current stakeholders, including firm management, valuation model outcomes may differ widely. Not only may these effects result in observed Enterprise Values that differs from the calculated outcome of a valuation model, but we may also see differing outcomes using the same valuation model applied to a particular firm.

The artistry lies in the ability to both interpret model outcomes and divine model inputs from a dizzying array of values and variables relative to any particular firm. It’s often suggested to students of Finance that a well-trained monkey and an iPad may currently perform relevant finance functions for a firm. While this high tech/low intellect combination may warrant minimal recompense in the capital and labor markets, talented and capable financiers often receive annual incomes measured in the hundreds of thousands or millions of dollars. Why the difference between the low cost monkey/iPad combination and the highly compensated financier labor form? Artistry and intuition.

[1] Prepared by Richard Haskell, PhD (2017), Associate Professor of Finance, Bill & Vieve Gore School of Business, Westminster College, Salt Lake City, Utah, rhaskell@westminstercollege.edu, www.richardhaskell.net

[2] Shrieves, R., and J Wachowicz (2001), Free Cash Flow, Economic Value Added, and Net Present Value: A reconciliation of variations of discounted-cash-flow valuation, The Engineering Economist, Vol. 46, No. 1, pg 33-52, 2001

[3] Discounted cash flow models generally produce consistently positive outcomes based on the condition ROIC > WACC > g. When a firm presents with a different generalized condition certain models may not be credible instruments for estimating the firm’s value

[4] “Animal spirits” is a term emphasizing the importance of investor sentiment on the market value of a firm’s debt and equity components. J.M. Keynes, General Theory of Employment, Interest and Money, pp 161-162, McMillan, London, 1936

Key Value Driver Model

Free Cash Flow Model [1]

Model Form

VALFCF

Inputs

| Free Cash Flow (FCF) |  |

| Long-Run Growth Rate of Cash Flow Variable (g) |

Long-run growth rates of the income variable (g = IR x ROIC and g = %  GDP) are used in the Continuing Value portion of the valuation models. GDP) are used in the Continuing Value portion of the valuation models. |

| Weighted Average Cost of Capital (Market Based) |

|

Description

Among discounted cash flow models, those using Free Cash Flow (FCF) as the cash flow variable are most commonly used by analysts and practitioners. FCF is considered by some to be a more reliable performance measure than other income variables. It is also more reflective of the cash flow form for which the owners of the firm’s capital structure hold future rights. Further, FCF may be dis-aggregated such that it’s possible to focus specifically on the operational structure of the firm.

The advantage to this approach is obvious in that it allows for the calculation of a firm’s value based on that which the firm produces for its debt and equity stakeholders: free cash flow. The FCF valuation model considers the firm’s weighted average cost of capital (WACC) as the discounting factor and like other discounted cash flow models in this study is comprised of the sum of the present value of the discounted cash flows over an explicit forecast period and the present value of the firm’s continuing value using a Free Cash Flow augmented form of the Dividend Yield model.

Though technically robust, the continuing value portion of this model form includes a structural weakness observable when the firm’s WACC is less than its g, resulting in a negative denominator and almost certainly a negative outcome for the continuing value term; unless the cash flow variable in the numerator is also negative. This condition results in a spurious valuation, regardless of the length of the explicit forecast period.

[1] Prepared by Richard Haskell, PhD [2017], (Associate Professor of Finance, Bill & Vieve Gore School of Business, Westminster College, Salt Lake City, Utah, rhaskell@westminstercollege.edu, www.richardhaskell.net) and Beau Lewis [2017], (Undergraduate Research Associate, Finance, Bill and Vieve Gore School of Business, Westminster College, Salt Lake City, Utah, https://www.linkedin.com/in/beau-lewis-5068a5120)

Economic Profit Model

Adjusted Present Value Model[1]

Model Form

VALAPV

Inputs

| Free Cash Flow (FCF) |  |

| Tax Shield (TS) |  |

| Long-Run Growth Rate of Cash Flow Variable (g) |

Long-run growth rates of the income variable (g = IR x ROIC and g = % GDP) are used in the Continuing Value portion of the valuation models. |

| Unlevered Cost of Equity Capital (ku) | This study employs the simplifying assumption that ku = kd = ktax = WACC |

| Weighted Average Cost of Capital (Market Based) |

|

Description

The Adjusted Present Value (APV) model takes into account the net present value of a firm asset inclusive of the valuation effects resulting from the firm’s choice of capital structures. It combines a Free Cash Flow valuation using the unlevered cost of equity (kU) as its discount rate and a valuation using the firm’s tax shield (TS) arising from the interest costs associated with the firm’s debt capital using the firm’s opportunity cost of funds used to pay taxes as the discount rate (ktax).

A primary purpose of this model form is to highlight changes in value as a function of changes in the firm’s capital structure, allowing for modeling with varying combinations of debt and equity capital. Though not expressly unique in this purpose, the APV model is the only one of the major discounted cash flow models to offer this perspective and is often used by practitioners seeking to present the case that the manner in which a firm is capitalized directly impacts the firm’s value.[2]

The APV model separates the value of forecasted free cash flows from the forecasted tax shields based on the premise that a tax shield (reduction of tax liability as the result of a tax deductible interest expense) has a similar effect on firm value as some other cash flow. The two segments of the equation, referred to commonly as VFCF and VTAX are presented as follows:

VALAPV = VALFCF + VALTAX

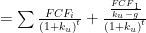

VALFCF

VALAPV

The model uses a classic summative present value of the discounted cash flows added to the present value of the continuing value of the same cash flow form based on a cash flow augmented form of the Dividend Yield Model. This model form is employed using both the subject firm’s Free Cash Flow and Tax Shield, summed to form an Adjusted Present Value valuation.

Though technically robust, the continuing value portion of this model form includes a structural weakness observable when the firm’s WACC is less than g, resulting in a negative denominator and almost certainly a negative outcome for the continuing value term; unless the cash flow variable in the numerator is also negative. This condition results in a spurious valuation, regardless of the length of the explicit forecast period.

In this construction, an assumption of ku = kd (the levered cost of firm debt capital) is aligned with the firm having a constant debt to equity ratio, while an assumption of ku = ktax suggests a non-constant debt to equity ratio[3]. It’s important to note that the g in the continuing value equations represent the growth rate of the relevant cash flow variable.

[1] Prepared by Richard Haskell, PhD [2017], (Associate Professor of Finance, Bill & Vieve Gore School of Business, Westminster College, Salt Lake City, Utah, rhaskell@westminstercollege.edu, www.richardhaskell.net) and Beau Lewis [2017], (Undergraduate Research Associate, Finance, Bill and Vieve Gore School of Business, Westminster College, Salt Lake City, Utah, https://www.linkedin.com/in/beau-lewis-5068a5120)

[2] This is in direct contrast with the Modigliani and Miller Theorem in which the firm’s capital structure is said to have no impact on the firm’s value. This section of the theorem includes the assumption that interest and corporate income tax rates are held constant at 0%.

[3] These assumptions arise from the Modigliani and Miller Theorem; Koller, T. Goedhart, M.H, Wessels, D., & Copeland, T.E.(2010), Valuation: Measuring and managing the value of companies (5th Edition), pg. 122, Hoboken, NJ, John Wiley & Sons

Forward Market Multiple Model