Johnson & Johnson

Analyst Listing

The following analysts provide coverage for the subject firm as of May 2016:

| Broker | Analyst | Analyst Email |

| Morningstar | Damien Conover | damien.conover@morningstar.com |

| BTIG | Dane Leone | dleone@btig.com |

| Leerink Partners | Danielle Antalffy | danielle.antalffy@leerink.com |

| Argus Research | David Toung | dtoung@argusresearch.com |

| Societe Generale | Florent Cespedes | florent.cespedes@sgcib.com |

| RBC Capital Markets | Glenn Novarro | glenn.novarro@rbccm.com |

| Raymond James | Jayson Bedford | jayson.bedford@raymondjames.com |

| Jefferies | Jeffrey Holford | jholford@jefferies.com |

| BMO Capital Markets | Joanne K. Wuensch | joanne.wuensch@bmo.com |

| Cowen & Company | Joshua Jennings | josh.jennings@cowen.com |

| Deutsche Bank Research | Kristen Stewart | kristen.stewart@db.com |

| Wells Fargo Securities | Larry Biegelsen | lawrence.biegelsen@wellsfargo.com |

| Piper Jaffray | Richard J. Purkiss | richard.j.purkiss@pjc.com |

| Stifel Nicolaus | Rick Wise | danielle.antalffy@leerink.com |

| Erste Group | Stephan Lingnau | stephan.lingnau@erstegroup.com |

| Atlantic Equities | Steve Chesney | s.chesney@atlantic-equities.com |

| Guggenheim Securities | Tony Butler | tony.butler@guggenheimpartners.com |

| Credit Suisse | Vamil Divan | vamil.divan@credit-suisse.com |

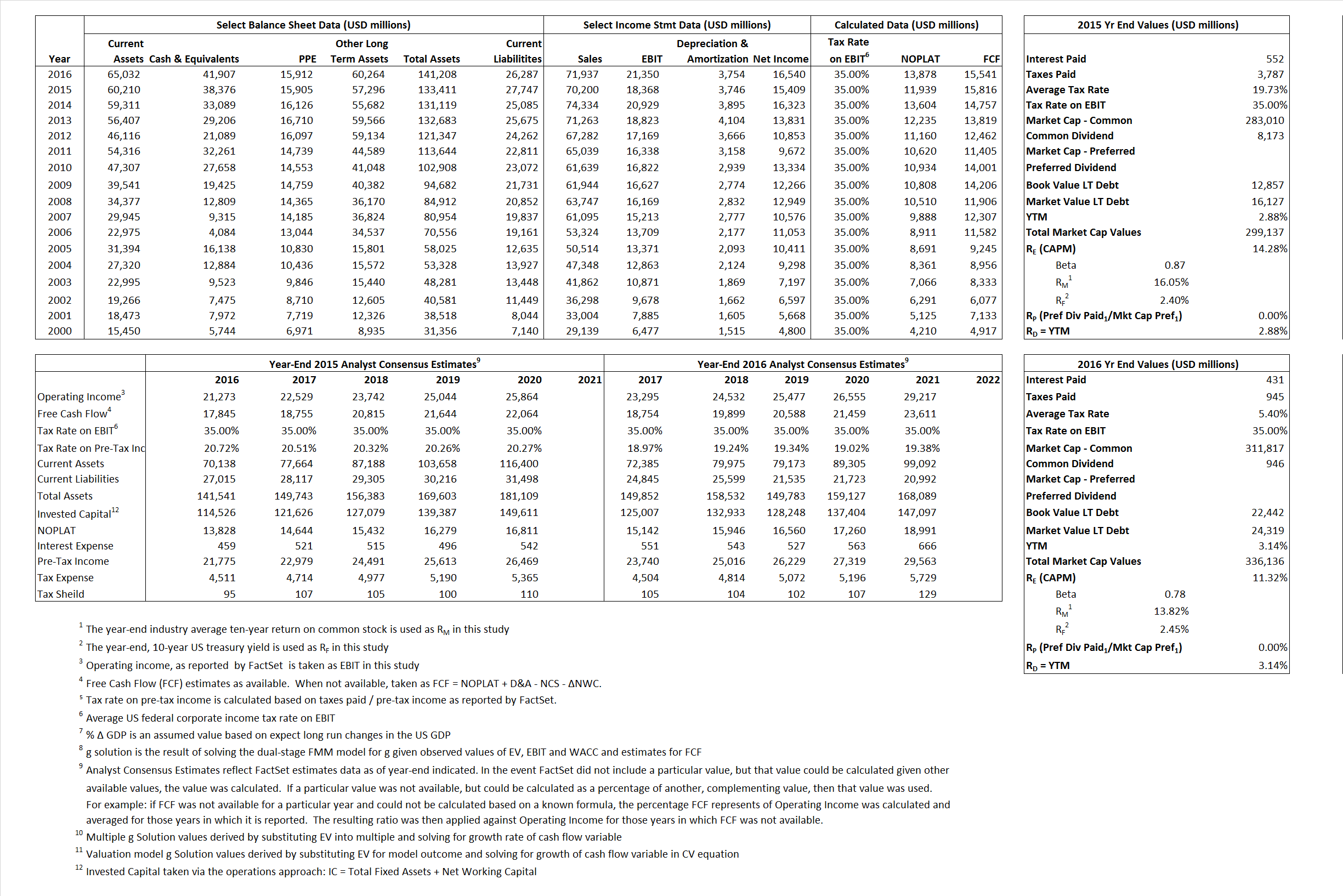

Primary Input Data

Derived Input Data

Derived Input |

Label |

2015 Value |

2016

|

Equational Form |

| Net Operating Profit Less Adjusted Taxes | NOPLAT | 11,939 | 13,878 |  |

| Free Cash Flow | FCF | 15,816 | 15,541 |  |

| Tax Shield | TS | 109 | 23 |  |

| Invested Capital | IC | 105,664 | 114,921 |  |

| Return on Invested Capital | ROIC | 11.30% | 12.08% |  |

| Net Investment | NetInv | 3,376 | 13,011 |  |

| Investment Rate | IR | 28.28% | 93.76% |  |

| Weighted Average Cost of Capital |

WACCMarket | 13.63% | 10.71% |  |

| WACCBook | 8.01% | 7.10% | ||

| Enterprise value |

EVMarket | 260,761 | 294,229 |  |

| EVBook | 253,960 | 292,352 | ||

| Long-Run Growth |

g = IR x ROIC |

3.20% | 11.32% | Long-run growth rates of the income variable are used in the Continuing Value portion of the valuation models. |

g = %  GDP GDP |

2.50% | 2.50% | ||

| Margin from Operations | M | 26.17% | 29.68% |  |

| Depreciation/Amortization Rate | D | 16.94% | 14.95% |  |

Valuation Multiple Outcomes

The outcomes presented in this study are the result of original input data, derived data, and synthesized inputs.

Equational Form |

Observed Value |

Single-stagemultiple g solution |

Two-stage valuationmodel g solution |

|||

| 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | |

|

|

3.71 | 4.09 | 15.22% | 9.84% | 14.59% | 10.30% |

|

|

11.79 | 11.72 | 15.22% | 9.84% | 14.59% | 10.30% |

|

|

21.84 | 21.20 | 15.22% | 9.84% | 14.59% | 10.30% |

|

|

16.49 | 18.93 | 15.22% | 9.84% | 14.59% | 10.30% |

|

|

14.20 | 13.78 | 15.22% | 9.84% | 14.59% | 10.30% |

|

|

2.47 | 2.56 | 15.22% | 9.84% | 14.59% | 10.30% |