United Parcel Service Inc

Analyst Listing

The following analysts provide coverage for the subject firm as of May 2016:

| Broker | Analyst | Analyst Email |

| Credit Suisse | Allison M. Landry | allison.landry@credit-suisse.com |

| Raymond James | Arthur W. Hatfield | art.hatfield@raymondjames.com |

| Susquehanna Financial Group | Bascome Majors | bascome.majors@sig.com |

| Stifel Nicolaus | David G. Ross | dross@stifel.com |

| Bernstein Research | David Vernon | david.vernon@bernstein.com |

| Avondale Partners | Donald Broughton | dbroughton@avondalepartnersllc.com |

| Cowen & Company | Helane Becker | helane.becker@cowen.com |

| Stephens Inc | Jack Atkins | jack.atkins@stephens.com |

| Buckingham Research | Jeffrey Kauffman | jkauffman@buckresearch.com |

| RBC Capital Markets | John Barnes | john.barnes@rbccm.com |

| BB&T Capital Markets | Kevin W. Sterling | ksterling@bbandtcm.com |

| Nomura Research | Matt Troy | matt.troy@nomura.com |

| William Blair | Nathan Brochmann | nbrochmann@williamblair.com |

| Deutsche Bank Research | Robert Salmon | robert.salmon@db.com |

| Wolfe Research | Scott H. Group | sgroup@wolferesearch.com |

| Oppenheimer | Scott Schneeberger | scott.schneeberger@opco.com |

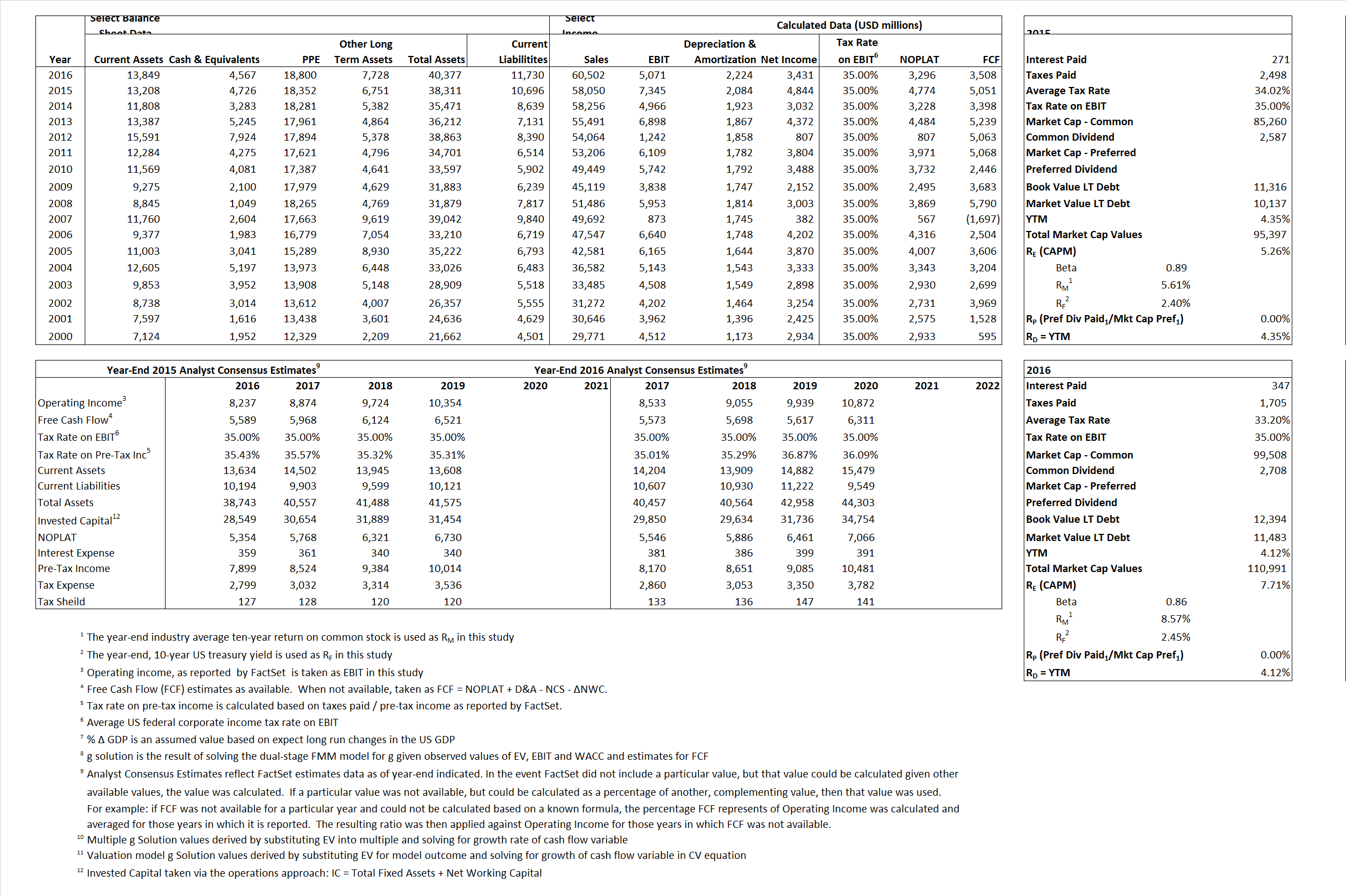

Primary Input Data

Derived Input Data

Derived Input |

Label |

2015 Value |

2016

|

Equational Form |

| Net Operating Profit Less Adjusted Taxes | NOPLAT | 4,774 | 3,296 |  |

| Free Cash Flow | FCF | 5,051 | 4,774 |  |

| Tax Shield | TS | 92 | 115 |  |

| Invested Capital | IC | 27,615 | 28,647 |  |

| Return on Invested Capital | ROIC | 17.29% | 11.51% |  |

| Net Investment | NetInv | 2,867 | 3,256 |  |

| Investment Rate | IR | 60.05% | 98.78% |  |

| Weighted Average Cost of Capital |

WACCMarket | 5.00% | 7.20% |  |

| WACCBook | 7.62% | 7.17% | ||

| Enterprise value |

EVMarket | 90,671 | 106,424 |  |

| EVBook | 92,009 | 107,335 | ||

| Long-Run Growth |

g = IR x ROIC |

10.38% | 11.37% | Long-run growth rates of the income variable are used in the Continuing Value portion of the valuation models. |

g = %  GDP GDP |

2.50% | 2.50% | ||

| Margin from Operations | M | 12.65% | 8.38% |  |

| Depreciation/Amortization Rate | D | 22.10% | 30.49% |  |

Valuation Multiple Outcomes

The outcomes presented in this study are the result of original input data, derived data, and synthesized inputs.

Equational Form |

Observed Value |

Single-stagemultiple g solution |

Two-stage valuationmodel g solution |

|||

| 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | |

|

|

1.56 | 1.76 | -0.38% | 5.61% | -0.99% | 6.10% |

|

|

9.62 | 14.59 | -0.38% | 5.61% | -0.99% | 6.10% |

|

|

18.99 | 32.29 | -0.38% | 5.61% | -0.99% | 6.10% |

|

|

17.95 | 30.34 | -0.38% | 5.61% | -0.99% | 6.10% |

|

|

12.34 | 20.99 | -0.38% | 5.61% | -0.99% | 6.10% |

|

|

3.28 | 3.72 | -0.38% | 5.61% | -0.99% | 6.10% |