Raytheon Company

Analyst Listing

The following analysts provide coverage for the subject firm as of May 2016:

| Broker | Analyst | Analyst Email |

| Cowen & Company | Cai Von Rumohr | cai.von-rumohr@cowen.com |

| Bernstein Research | Douglas S. Harned | douglas.harned@bernstein.com |

| Jefferies | Howard A. Rubel | hrubel@jefferies.com |

| Wolfe Research | Hunter K. Keay | hkeay@wolferesearch.com |

| Stifel Nicolaus | Jospeh W. DeNardi | denardij@stifel.com |

| Deutsche Bank Research | Myles Walton | myles.walton@db.com |

| CRT Capital Group | Peter Arment | parment@sterneageecrt.com |

| Drexel Hamilton | Peteral Skibitski | pskibitski@drexelhamilton.com |

| Buckingham Research | Richard Safran | rsafran@buckresearch.com |

| Credit Suisse | Robert Spingarn | robert.spingarn@credit-suisse.com |

| RBC Capital Markets | Robert Stallard | robert.stallard@rbccm.com |

| Guggenheim Securities | Roman Schwizer | roman.schweizer@guggenheimpartners.com |

| Wells Fargo Securties | Sam J. Pearlstein | sam.pearlstein@wellsfargo.com |

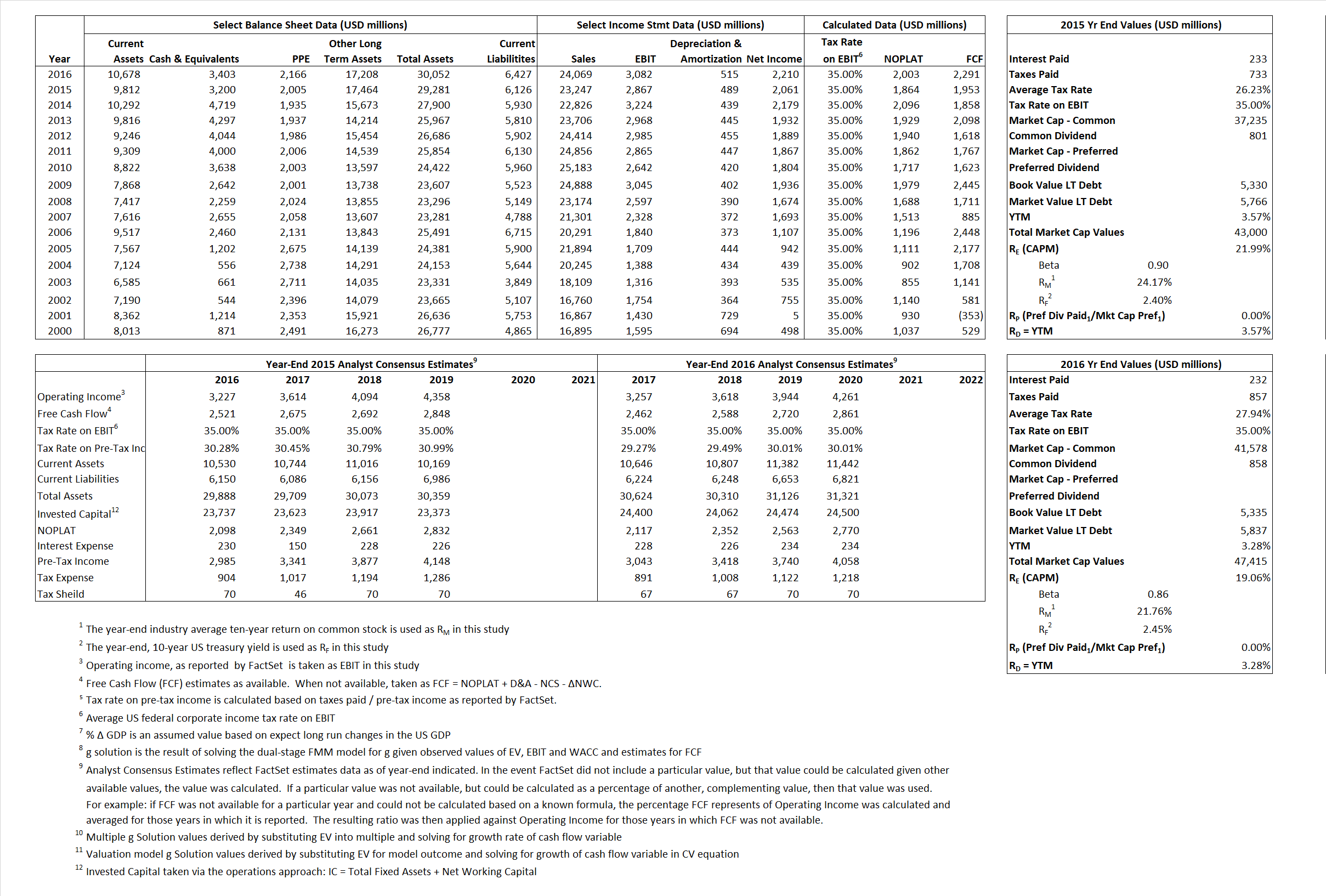

Primary Input Data

Derived Input Data

Derived Input |

Label |

2015 Value |

2016

|

Equational Form |

| Net Operating Profit Less Adjusted Taxes | NOPLAT | 1,864 | 2,003 |  |

| Free Cash Flow | FCF | 1,953 | 2,291 |  |

| Tax Shield | TS | 61 | 65 |  |

| Invested Capital | IC | 23,155 | 23,625 |  |

| Return on Invested Capital | ROIC | 8.05% | 8.48% |  |

| Net Investment | NetInv | 1,674 | 985 |  |

| Investment Rate | IR | 89.83% | 49.17% |  |

| Weighted Average Cost of Capital |

WACCMarket | 19.40% | 17.00% |  |

| WACCBook | 7.86% | 7.37% | ||

| Enterprise value |

EVMarket | 39,800 | 44,012 |  |

| EVBook | 39,162 | 43,510 | ||

| Long-Run Growth |

g = IR x ROIC |

7.23% | 4.17% | Long-run growth rates of the income variable are used in the Continuing Value portion of the valuation models. |

g = %  GDP GDP |

2.50% | 2.50% | ||

| Margin from Operations | M | 12.33% | 12.80% |  |

| Depreciation/Amortization Rate | D | 14.57% | 14.32% |  |

Valuation Multiple Outcomes

The outcomes presented in this study are the result of original input data, derived data, and synthesized inputs.

Equational Form |

Observed Value |

Single-stagemultiple g solution |

Two-stage valuationmodel g solution |

|||

| 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | |

|

|

1.71 | 1.83 | 35.18% | 26.88% | 25.43% | 20.42% |

|

|

11.86 | 12.24 | 35.18% | 26.88% | 25.43% | 20.42% |

|

|

21.36 | 21.97 | 35.18% | 26.88% | 25.43% | 20.42% |

|

|

20.38 | 19.21 | 35.18% | 26.88% | 25.43% | 20.42% |

|

|

13.88 | 14.28 | 35.18% | 26.88% | 25.43% | 20.42% |

|

|

1.72 | 1.86 | 35.18% | 26.88% | 25.43% | 20.42% |