Home Depot, Inc.

Analyst Listing

The following analysts provide coverage for the subject firm as of May 2016:

| Broker | Analyst | Analyst Email |

| Longbow Research | David S. MacGregor | dmacgregor@longbowresearch.com |

| Evercore ISI | Greg Melich | greg.melich@evercoreisi.com |

| RBC Capital Markets | Scot Ciccarelli | scot.ciccarelli@rbccm.com |

| Deutsche Bank Research | Mike Baker | michael.baker@db.com |

| Telsey Advisory Group | Joseph Feldman | jfeldman@telseygroup.com |

| Piper Jaffray | Peter J. Keith | peter.j.keith@pjc.com |

| Nomura Research | Jessica A. Schoen | jessica.schoen@nomura.com |

| Consumer Edge Research | David A. Schick | dschick@consumeredgeresearch.com |

| Atlantic Equities | Sam Hudson | s.hudson@atlantic-equities.com |

| Credit Suisse | Seth Sigman | seth.sigman@credit-suisse.com |

| SunTrust Robinson Humphrey | Keith Hughes | keith.hughes@suntrust.com |

| Oppenheimer | Brian Nagel | brian.nagel@opco.com |

| Wolfe Research | Scott Mushkin | smushkin@wolferesearch.com |

| Daiwa Securities Co. Ltd. | Kahori Tamada | kahori.tamada@us.daiwacm.com |

| Wedbush Securities | Seth Basham | seth.basham@wedbush.com |

| Jefferies | Daniel Binder | dbinder@jefferies.com |

| Raymond James | Budd Bugatch | budd.bugatch@raymondjames.com |

| BMO Capital Markets | Wayne Hood | wayne.hood@bmo.com |

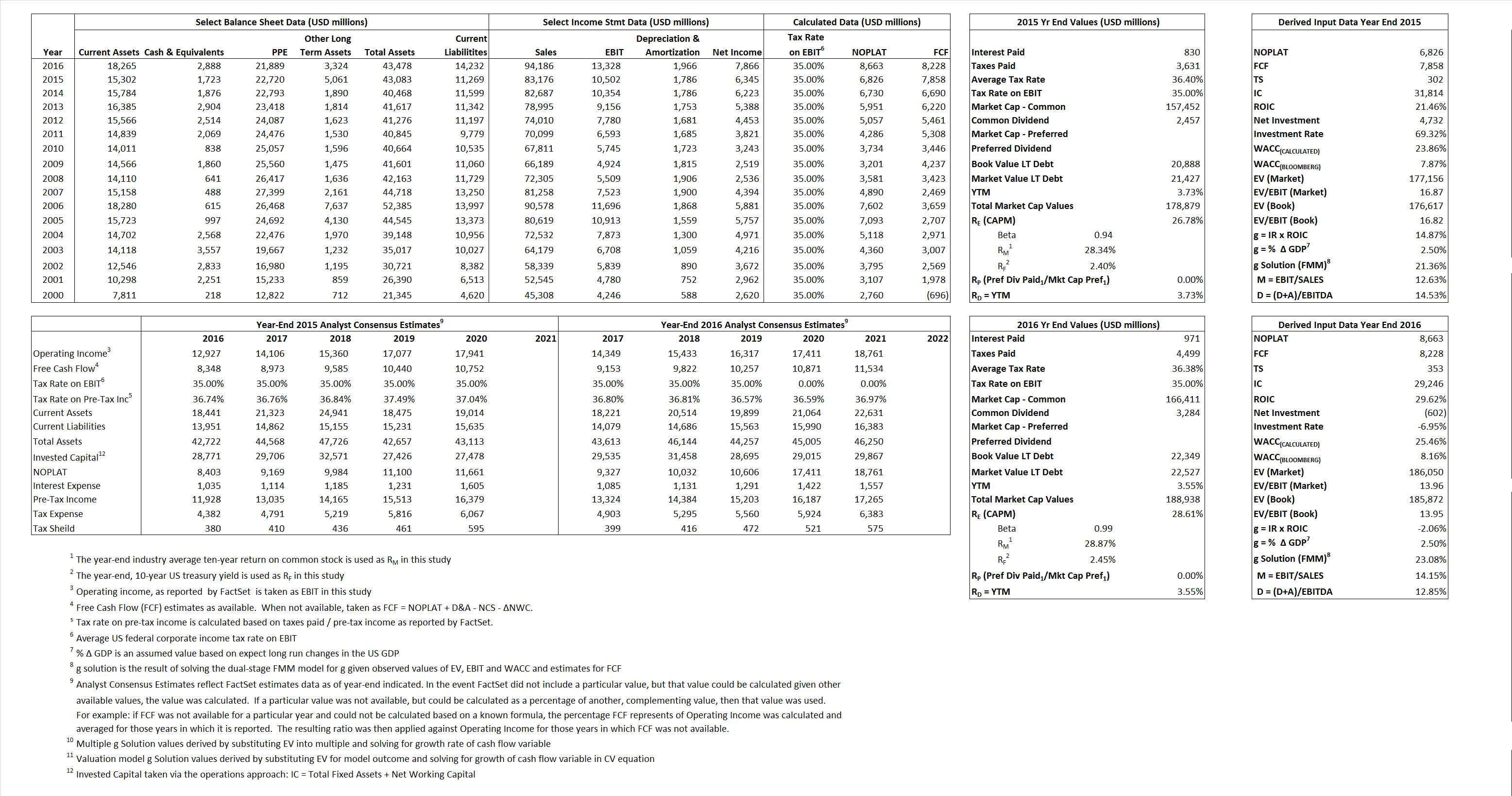

Primary Input Data

Derived Input Data

Derived Input |

Label |

2015 Value |

2016

|

Equational Form |

| Net Operating Profit Less Adjusted Taxes | NOPLAT | 6,826 | 8,663 |  |

| Free Cash Flow | FCF | 7,858 | 8,228 |  |

| Tax Shield | TS | 302 | 353 |  |

| Invested Capital | IC | 31,814 | 29,246 |  |

| Return on Invested Capital | ROIC | 21.46% | 29.62% |  |

| Net Investment | NetInv | 4,732 | (602) |  |

| Investment Rate | IR | 69.32% | -6.95% |  |

| Weighted Average Cost of Capital |

WACCMarket | 23.86% | 25.46% |  |

| WACCBook | 7.87% | 8.16% | ||

| Enterprise value |

EVMarket | 117,1156 | 186,050 |  |

| EVBook | 176,617 | 185,872 | ||

| Long-Run Growth |

g = IR x ROIC |

14.87% | -2.06% | Long-run growth rates of the income variable are used in the Continuing Value portion of the valuation models. |

g = %  GDP GDP |

2.50% | 2.50% | ||

| Margin from Operations | M | 12.63% | 14.15% |  |

| Depreciation/Amortization Rate | D | 14.53% | 12.85% |  |

Valuation Multiple Outcomes

The outcomes presented in this study are the result of original input data, derived data, and synthesized inputs.

Equational Form |

Observed Value |

Single-stagemultiple g solution |

Two-stage valuationmodel g solution |

|||

| 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | |

|

|

2.13 | 1.98 | 24.39% | 24.69% | 24.05% | 25.24% |

|

|

14.42 | 12.16 | 24.39% | 24.69% | 24.05% | 25.24% |

|

|

25.95 | 21.48 | 24.39% | 24.69% | 24.05% | 25.24% |

|

|

22.54 | 22.61 | 24.39% | 24.69% | 24.05% | 25.24% |

|

|

16.87 | 13.96 | 24.39% | 24.69% | 24.05% | 25.24% |

|

|

5.57 | 6.36 | 24.39% | 24.69% | 24.05% | 25.24% |