Dow Chemical Company

Analyst Listing

The following analysts provide coverage for the subject firm as of May 2016:

| Broker | Analyst | Analyst Email |

| Nomura Research | Aleksey Yefremov | aleksey.yefremov@nomura.com |

| RBC Capital Markets | Arun Viswanathan | arun.viswanathan@rbccm.com |

| Credit Suisse | Christopher S. Parkinson | christopher.parkinson@credit-suisse.com |

| Deutsche Bank Research | David Begleiter | david.begleiter@db.com |

| Susquehanna Financial Group | Don Carson | don.carson@sig.com |

| Wells Fargo Securities | Frank J. Mitsch | frank.mitsch@wellsfargo.com |

| Monness Crespi Hardt | Herbert Hardt | hhardt@mchny.com |

| SunTrust Robinson Humphrey | James Sheehan | james.sheehan@suntrust.com |

| Jefferies | Laurence Alexander | lalexander@jefferies.com |

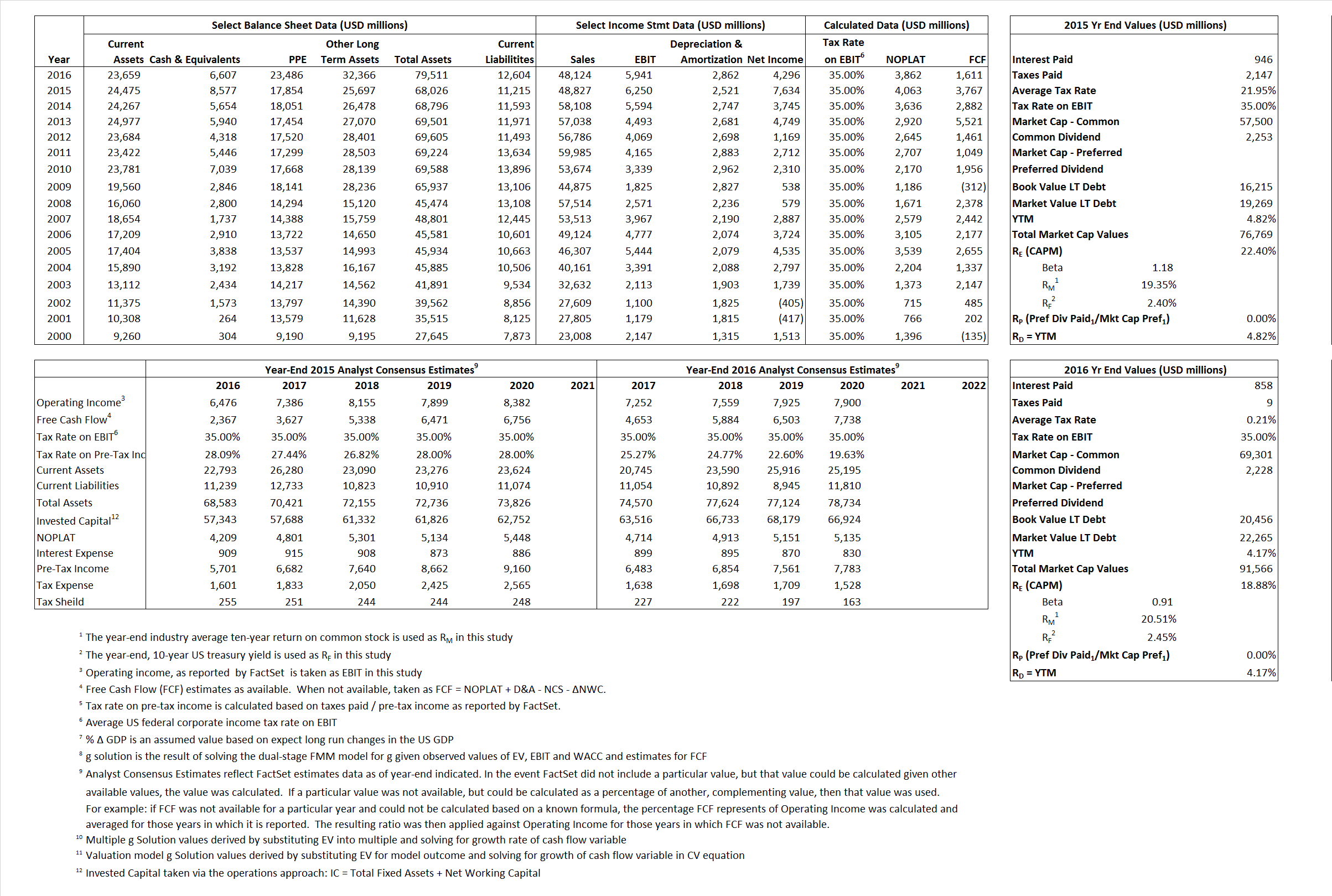

Primary Input Data

Derived Input Data

Derived Input |

Label |

2015 Value |

2016

|

Equational Form |

| Net Operating Profit Less Adjusted Taxes | NOPLAT | 4,063 | 3,862 |  |

| Free Cash Flow | FCF | 3,767 | 1,611 |  |

| Tax Shield | TS | 208 | 2 |  |

| Invested Capital | IC | 56,811 | 66,907 |  |

| Return on Invested Capital | ROIC | 7.15% | 5.77% |  |

| Net Investment | NetInv | 2,129 | 12,958 |  |

| Investment Rate | IR | 52.41% | 333.56% |  |

| Weighted Average Cost of Capital |

WACCMarket | 17.72% | 15.30% |  |

| WACCBook | 8.79% | 7.21% | ||

| Enterprise value |

EVMarket | 68,192 | 84,959 |  |

| EVBook | 65,138 | 83,150 | ||

| Long-Run Growth |

g = IR x ROIC |

3.75% | 19.37% | Long-run growth rates of the income variable are used in the Continuing Value portion of the valuation models. |

g = %  GDP GDP |

2.50% | 2.50% | ||

| Margin from Operations | M | 12.80% | 12.35% |  |

| Depreciation/Amortization Rate | D | 28.74% | 32.51% |  |

Valuation Multiple Outcomes

The outcomes presented in this study are the result of original input data, derived data, and synthesized inputs.

Equational Form |

Observed Value |

Single-stagemultiple g solution |

Two-stage valuationmodel g solution |

|||

| 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | |

|

|

1.40 | 1.77 | 70.49% | 50.64% | 26.94% | 22.96% |

|

|

7.77 | 9.65 | 70.49% | 50.64% | 26.94% | 22.96% |

|

|

16.79 | 22.00 | 70.49% | 50.64% | 26.94% | 22.96% |

|

|

18.10 | 52.74 | 70.49% | 50.64% | 26.94% | 22.96% |

|

|

10.91 | 14.30 | 70.49% | 50.64% | 26.94% | 22.96% |

|

|

1.20 | 1.27 | 70.49% | 50.64% | 26.94% | 22.96% |