UnitedHealth Group Incorporated

Analyst Listing

The following analysts provide coverage for the subject firm as of May 2016:

| Broker | Analyst | Analyst Email |

| Leerink Partners | Ana Gupte | ana.gupte@leerink.com |

| CRT Capital Group | Brian Wright | bwright@sterneageecrt.com |

| Susquehanna Financial Group | Chris Rigg | chris.rigg@sig.com |

| Cowen & Company | Christine Arnold | christine.arnold@cowen.com |

| Jefferies | David Windley | dwindley@jefferies.com |

| RBC Capital Markets | Frank G. Morgan | frank.morgan@rbccm.com |

| Cantor Fitzgerald | Joseph D. France | jfrance@cantor.com |

| Raymond James | Michael J. Baker | michael.baker@raymondjames.com |

| Oppenheimer | Michael Wiederhorn | michael.wiederhorn@opco.com |

| Wells Fargo Securities | Peter Costa | peter.costa@wellsfargo.com |

| Wedbush Securities | Sarah James | sarah.james@wedbush.com |

| Credit Suisse | Scott Fidel | scott.fidel@credit-suisse.com |

| Piper Jaffray | Sean W. Wieland | sean.w.wieland@pjc.com |

| Mizuho Securities USA | Sheryl R. Skolnick | sheryl.skolnick@us.mizuho-sc.com |

| FBR Capital Markets & Co | Steven Halper | shalper@fbr.com |

| Stifel Nicolaus | Thomas A. Carroll | tacarroll@stifel.com |

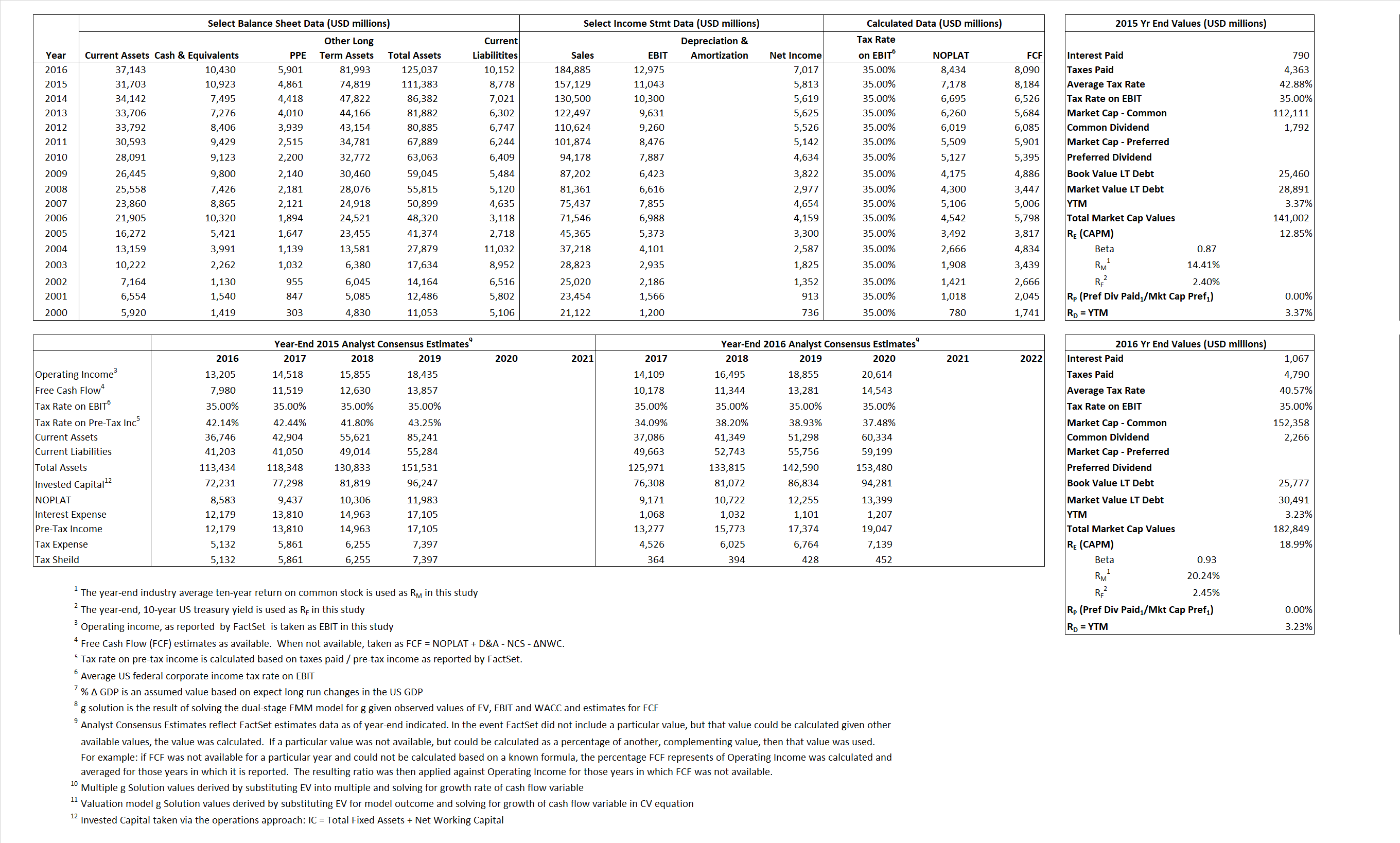

Primary Input Data

Derived Input Data

Derived Input |

Label |

2015 Value |

2016

|

Equational Form |

| Net Operating Profit Less Adjusted Taxes | NOPLAT | 7,178 | 8,434 |  |

| Free Cash Flow | FCF | 8,184 | 8,090 |  |

| Tax Shield | TS | 339 | 433 |  |

| Invested Capital | IC | 102,605 | 114,885 |  |

| Return on Invested Capital | ROIC | 7.00% | 7.34% |  |

| Net Investment | NetInv | 23,244 | 12,280 |  |

| Investment Rate | IR | 323.83% | 145.61% |  |

| Weighted Average Cost of Capital |

WACCMarket | 10.61% | 16.15% |  |

| WACCBook | 6.94% | 7.30% | ||

| Enterprise value |

EVMarket | 130,079 | 172,419 |  |

| EVBook | 127,141 | 167,705 | ||

| Long-Run Growth |

g = IR x ROIC |

22.65% | 10.69% | Long-run growth rates of the income variable are used in the Continuing Value portion of the valuation models. |

g = %  GDP GDP |

2.50% | 2.50% | ||

| Margin from Operations | M | 7.03% | 7.02% |  |

| Depreciation/Amortization Rate | D | 0.00% | 0.00% |  |

Valuation Multiple Outcomes

The outcomes presented in this study are the result of original input data, derived data, and synthesized inputs.

Equational Form |

Observed Value |

Single-stagemultiple g solution |

Two-stage valuationmodel g solution |

|||

| 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | |

|

|

0.83 | 0.93 | 24.11% | 33.37% | 20.03% | 21.23% |

|

|

11.78 | 13.29 | 24.11% | 33.37% | 20.03% | 21.23% |

|

|

18.12 | 20.44 | 24.11% | 33.37% | 20.03% | 21.23% |

|

|

15.89 | 21.31 | 24.11% | 33.37% | 20.03% | 21.23% |

|

|

11.78 | 13.29 | 24.11% | 33.37% | 20.03% | 21.23% |

|

|

1.27 | 1.50 | 24.11% | 33.37% | 20.03% | 21.23% |