Target Corporation

Analyst Listing

The following analysts provide coverage for the subject firm as of May 2016:

| Broker | Analyst | Analyst Email |

| Jefferies | Daniel Binder | dbinder@jefferies.com |

| Consumer Edge Research | David A. Schick | dschick@consumeredgeresearch.com |

| Evercore ISI | Greg Melich | greg.melich@evercoreisi.com |

| Cowen & Company | Jason H. Seidl | jason.seidl@cowen.com |

| Buckingham Research | John Zolidis | jzolidis@buckresearch.com |

| Telsey Advisory Group | Joseph Feldman | jfeldman@telseygroup.com |

| Daiwa Securities Co. Ltd. | Kahori Tamada | kahori.tamada@us.daiwacm.com |

| Credit Suisse | Michael Exstein | michael.exstein@credit-suisse.com |

| Deutsche Bank Research | Paul Trussell | paul.trussell@db.com |

| CRT Capital Group | Renato Basanta | rbasanta@sterneageecrt.com |

| Nomura Research | Robert S. Drbul | robert.drbul@nomura.com |

| Wolfe Research | Scott Mushkin | smushkin@wolferesearch.com |

| Piper Jaffray | Sean P. Naughton | sean.p.naughton@pjc.com |

| BMO Capital Markets | Wayne Hood | wayne.hood@bmo.com |

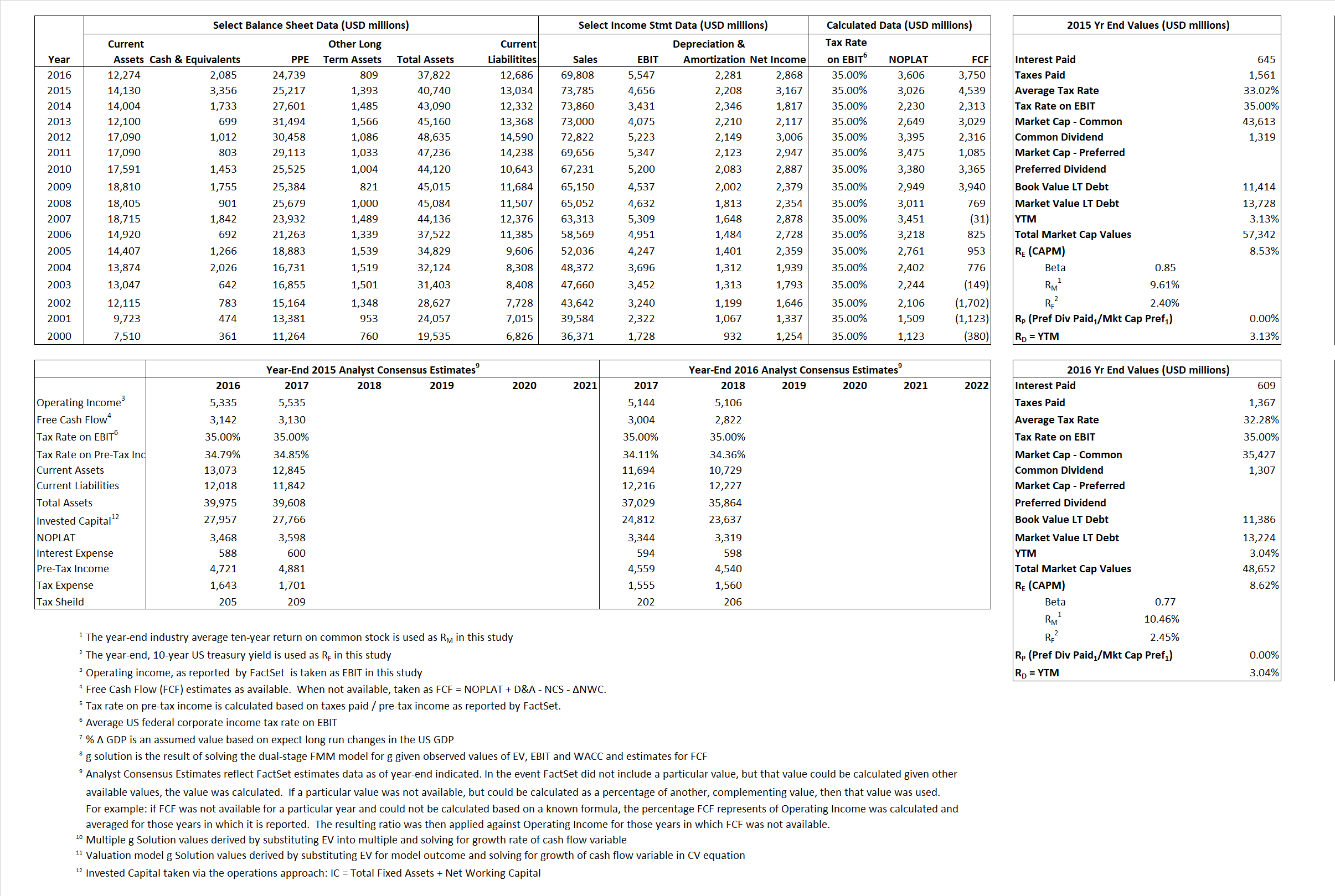

Primary Input Data

Derived Input Data

Derived Input |

Label |

2015 Value |

2016

|

Equational Form |

| Net Operating Profit Less Adjusted Taxes | NOPLAT | 3,026 | 3,606 |  |

| Free Cash Flow | FCF | 4,539 | 3,750 |  |

| Tax Shield | TS | 213 | 197 |  |

| Invested Capital | IC | 27,706 | 25,136 |  |

| Return on Invested Capital | ROIC | 10.92% | 14.34% |  |

| Net Investment | NetInv | (843) | (289) |  |

| Investment Rate | IR | -27.87% | -8.02% |  |

| Weighted Average Cost of Capital |

WACCMarket | 6.99% | 6.83% |  |

| WACCBook | 6.42% | 6.17% | ||

| Enterprise value |

EVMarket | 53,986 | 46,567 |  |

| EVBook | 52,942 | 44,728 | ||

| Long-Run Growth |

g = IR x ROIC |

-3.04% | -1.15% | Long-run growth rates of the income variable are used in the Continuing Value portion of the valuation models. |

g = %  GDP GDP |

2.50% | 2.50% | ||

| Margin from Operations | M | 6.31% | 7.95% |  |

| Depreciation/Amortization Rate | D | 32.17% | 29.14% |  |

Valuation Multiple Outcomes

The outcomes presented in this study are the result of original input data, derived data, and synthesized inputs.

Equational Form |

Observed Value |

Single-stagemultiple g solution |

Two-stage valuationmodel g solution |

|||

| 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | |

|

|

0.73 | 0.67 | 2.84% | -1.97% | 3.04% | 0.10% |

|

|

7.87 | 5.95 | 2.84% | -1.97% | 3.04% | 0.10% |

|

|

17.84 | 12.92 | 2.84% | -1.97% | 3.04% | 0.10% |

|

|

11.89 | 12.42 | 2.84% | -1.97% | 3.04% | 0.10% |

|

|

11.59 | 8.39 | 2.84% | -1.97% | 3.04% | 0.10% |

|

|

1.95 | 1.85 | 2.84% | -1.97% | 3.04% | 0.10% |