Medtronic Plc

Analyst Listing

The following analysts provide coverage for the subject firm as of May 2016:

| Broker | Analyst | Analyst Email |

| William Blair | Ben Andrew | bandrew@williamblair.com |

| Piper Jaffray | Brooks E. West | brooks.e.west@pjc.com |

| SunTrust Robinson Humphrey | Bruce Nudell | bruce.nudell@suntrust.com |

| Leerink Partners | Danielle Antalffy | danielle.antalffy@leerink.com |

| RBC Capital Markets | Glenn Novarro | glenn.novarro@rbccm.com |

| BMO Capital Markets | Joanne K. Wuensch | joanne.wuensch@bmo.com |

| Cowen & Company | Joshua Jennings | josh.jennings@cowen.com |

| Deutsche Bank Research | Kristen Stewart | kristen.stewart@db.com |

| Wells Fargo Securities | Larry Biegelsen | lawrence.biegelsen@wellsfargo.com |

| Credit Suisse | Matthew Keeler | matthew.keeler@credit-suisse.com |

| Needham | Mike Matson | mmatson@needhamco.com |

| Jefferies | Raj Denhoy | rdenhoy@jefferies.com |

| Stifel Nicolaus | Rick Wise | wiser@stifel.com |

| BTIG | Sean Lavin | slavin@btig.com |

| Oppenheimer | Steven Lichtman | steven.lichtman@opco.com |

| Wedbush Securities | Tao Levy | tao.levy@wedbush.com |

| Evercore ISI | Vijay Kumar | vijay.kumar@evercoreisi.com |

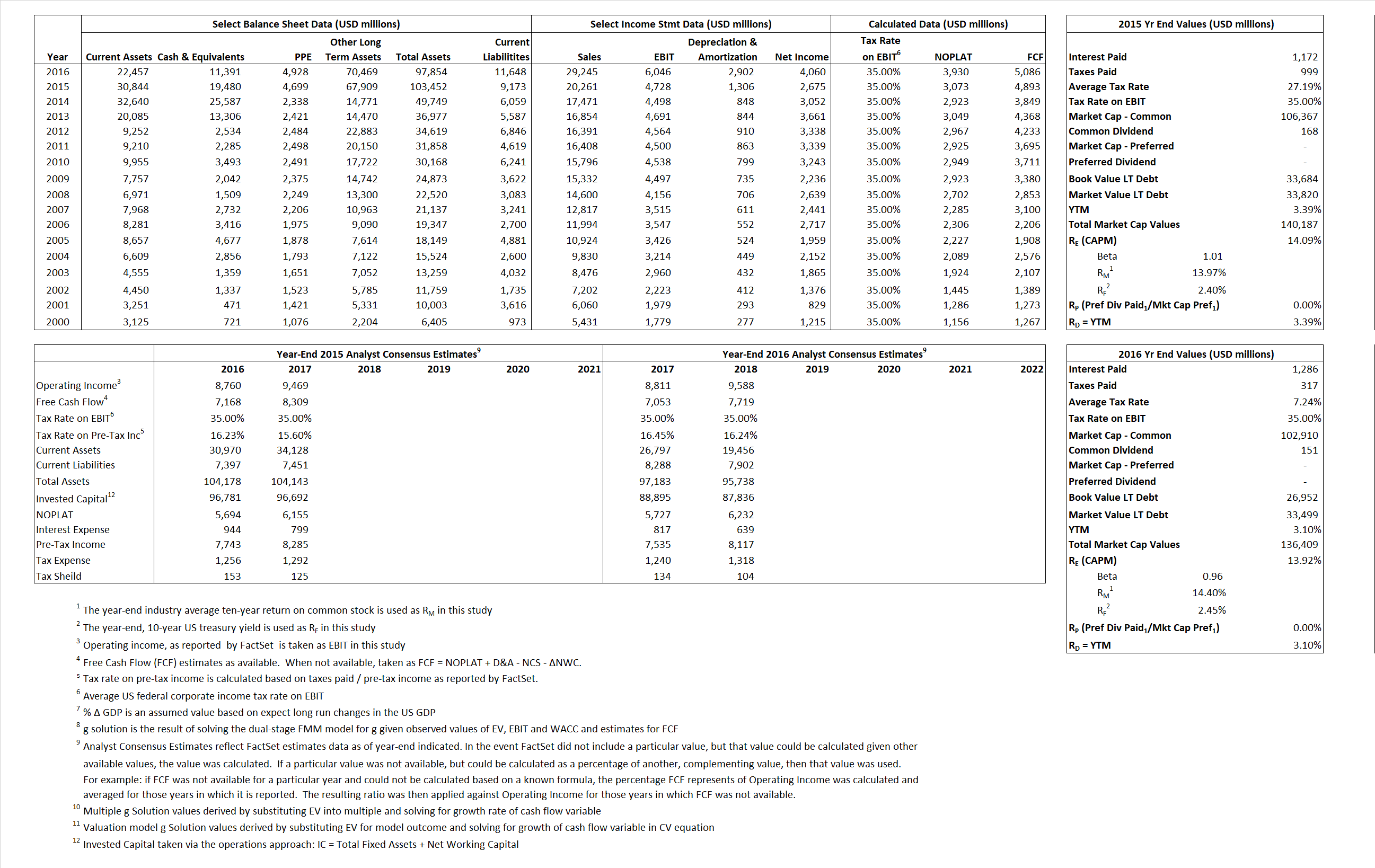

Primary Input Data

Derived Input Data

Derived Input |

Label |

2015 Value |

2016

|

Equational Form |

| Net Operating Profit Less Adjusted Taxes | NOPLAT | 3,073 | 3,930 |  |

| Free Cash Flow | FCF | 4,893 | 5,086 |  |

| Tax Shield | TS | 319 | 93 |  |

| Invested Capital | IC | 94,279 | 86,206 |  |

| Return on Invested Capital | ROIC | 3.26% | 4.56% |  |

| Net Investment | NetInv | 51,896 | (5,171) |  |

| Investment Rate | IR | 1,688.66% | -131.59% |  |

| Weighted Average Cost of Capital |

WACCMarket | 11.28% | 11.21% |  |

| WACCBook | 7.72% | 7.37% | ||

| Enterprise value |

EVMarket | 120,707 | 125,018 |  |

| EVBook | 128,660 | 118,471 | ||

| Long-Run Growth |

g = IR x ROIC |

55.04% | -6.00% | Long-run growth rates of the income variable are used in the Continuing Value portion of the valuation models. |

g = %  GDP GDP |

2.50% | 2.50% | ||

| Margin from Operations | M | 23.34% | 20.67% |  |

| Depreciation/Amortization Rate | D | 21.64% | 32.43% |  |

Valuation Multiple Outcomes

The outcomes presented in this study are the result of original input data, derived data, and synthesized inputs.

Equational Form |

Observed Value |

Single-stagemultiple g solution |

Two-stage valuationmodel g solution |

|||

| 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | |

|

|

5.96 | 4.27 | 39.91% | 25.98% | 30.72% | 19.59% |

|

|

20.00 | 13.97 | 39.91% | 25.98% | 30.72% | 19.59% |

|

|

39.28 | 31.81 | 39.91% | 25.98% | 30.72% | 19.59% |

|

|

24.67 | 24.58 | 39.91% | 25.98% | 30.72% | 19.59% |

|

|

35.53 | 20.68 | 39.91% | 25.98% | 30.72% | 19.59% |

|

|

1.28 | 1.45 | 39.91% | 25.98% | 30.72% | 19.59% |