Texas Instruments

Analyst Listing

The following analysts provide coverage for the subject firm as of May 2016:

| Broker | Analyst | Analyst Email |

| BMO Capital Markets | Ambrish Srivastava | ambrish.srivastava@bmo.com |

| RBC Capital Markets | Amit Daryanani | amit.daryanani@rbccm.com |

| Wedbush Securities | Betsy Van Hees | betsy.vanhees@wedbush.com |

| Evercore ISI | C.J. Muse | cj.muse@evercoreisi.com |

| Drexel Hamilton | Cody Acree | cacree@drexelhamilton.com |

| B Riley & Co | Craig A. Ellis | cellis@brileyco.com |

| Wells Fargo Securities | David Wong | david.m.wong@wellsfargo.com |

| CRT Capital Group | Douglas Freedman | dfreedman@sterneageecrt.com |

| Raymond James | J. Steven Smigie | steve.smigie@raymondjames.com |

| Credit Suisse | John Pitzer | john.pitzer@credit-suisse.com |

| Jefferies | Mark Lipacis | mlipacis@jefferies.com |

| Pacific Crest Securities-KBCM | Michael McConnell | mmcconnell@pacific-crest.com |

| Oppenheimer | Rick Schafer | rick.schafer@opco.com |

| Nomura Research | Romit Shah | romit.shah@nomura.com |

| Deutsche Bank Research | Ross Seymore | ross.seymore@db.com |

| Bernstein Research | Stacy A. Rasgon | stacy.rasgon@bernstein.com |

| Cowen & Company | Timothy Arcuri | timothy.arcuri@cowen.com |

| Stifel Nicolaus | Tore Svanberg | tsvanberg@stifel.com |

| Mizuho Securities USA | Vijay Rakesh | vijay.rakesh@us.mizuho-sc.com |

| SunTrust Robinson Humphrey | William Stein | william.stein@suntrust.com |

| Daiwa Securities Co. Ltd. | Yoko Yamada | yoko.yamada@us.daiwacm.com |

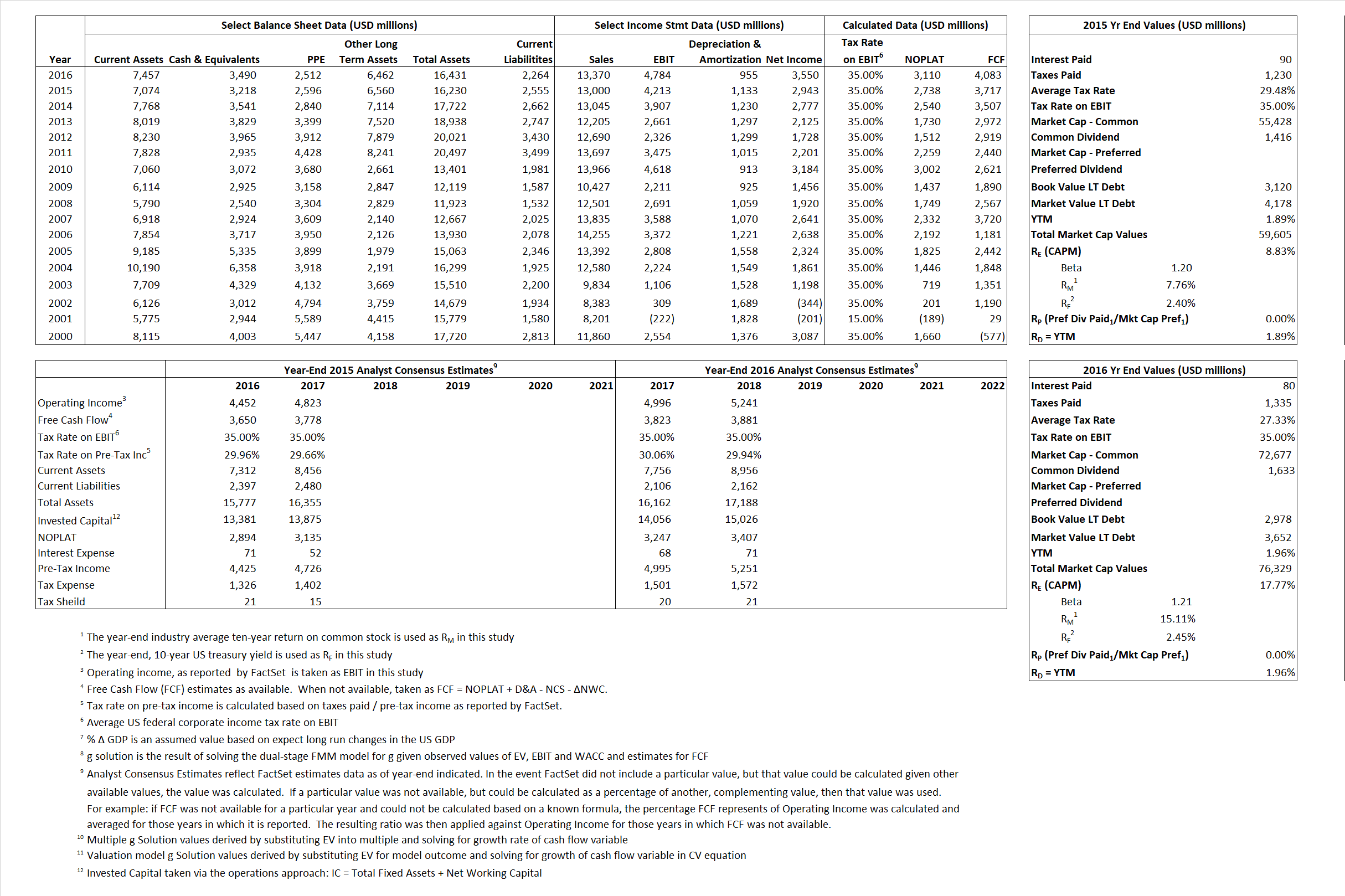

Primary Input Data

Derived Input Data

Derived Input |

Label |

2015 Value |

2016

|

Equational Form |

| Net Operating Profit Less Adjusted Taxes | NOPLAT | 2,738 | 3,110 |  |

| Free Cash Flow | FCF | 3,717 | 4,083 |  |

| Tax Shield | TS | 27 | 22 |  |

| Invested Capital | IC | 13,675 | 14,167 |  |

| Return on Invested Capital | ROIC | 20.03% | 21.95% |  |

| Net Investment | NetInv | (252) | 1,447 |  |

| Investment Rate | IR | -9.20% | 46.53% |  |

| Weighted Average Cost of Capital |

WACCMarket | 8.31% | 16.99% |  |

| WACCBook | 10.21% | 9.95% | ||

| Enterprise value |

EVMarket | 56,387 | 72,839 |  |

| EVBook | 55,058 | 72,165 | ||

| Long-Run Growth |

g = IR x ROIC |

-1.84% | 10.21% | Long-run growth rates of the income variable are used in the Continuing Value portion of the valuation models. |

g = %  GDP GDP |

2.50% | 2.50% | ||

| Margin from Operations | M | 32.41% | 35.78% |  |

| Depreciation/Amortization Rate | D | 21.19% | 16.64% |  |

Valuation Multiple Outcomes

The outcomes presented in this study are the result of original input data, derived data, and synthesized inputs.

Equational Form |

Observed Value |

Single-stagemultiple g solution |

Two-stage valuationmodel g solution |

|||

| 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | 12/31/2015 | 12/31/2016 | |

|

|

4.34 | 5.45 | 4.55% | 15.79% | 4.72% | 16.16% |

|

|

10.55 | 12.69 | 4.55% | 15.79% | 4.72% | 16.16% |

|

|

20.59 | 23.42 | 4.55% | 15.79% | 4.72% | 16.16% |

|

|

15.17 | 17.84 | 4.55% | 15.79% | 4.72% | 16.16% |

|

|

13.38 | 15.23 | 4.55% | 15.79% | 4.72% | 16.16% |

|

|

4.12 | 5.14 | 4.55% | 15.79% | 4.72% | 16.16% |